It keeps on raining downgrades in Australia. Week three of the local reporting season saw FNArena’s tally run up to 39 downgrades for individual ASX-listed stocks, and that’s just for the five trading sessions, against 19 upgrades. These numbers are not unprecedented, but they are high nevertheless, and they also reveal a heavy skew towards downgrades.

In most cases, valuation seems to be the culprit, but not always solely because of share price exuberance. There are numerous companies that remain simply unable to turn the ship decisively around, and analysts, like any other human, will lose their patience at some point.

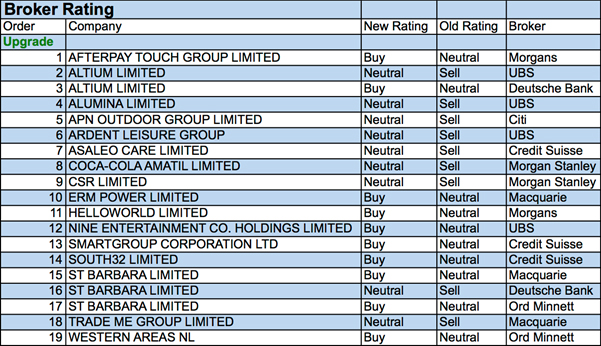

In the good books

ARDENT LEISURE GROUP (AAD) was upgraded to Neutral from Sell by UBS. B/H/S: 2/3/0 Ardent’s result was weak but well-flagged. Losses in theme parks were ongoing, and likely will be at least until the coronial inquiry wraps up in November. Impairments were taken on five Main Event sites in challenging locations and only one new site is flagged for FY19. UBS notes an improved outlook for Main Event margins given greater confidence in revenues. Target rises to $2.00 from $1.75.

[1]

[1]

AFTERPAY TOUCH GROUP LIMITED (APT) was upgraded to Add from Hold by Morgans. B/H/S: 2/0/0. Afterpay Touch’s FY18 result met fourth-quarter guidance, buoyed by strong US expansion. The company also announced plans to expand into the UK, a move the broker says will add to its potentially strong growth profile over several years. Morgans notes US sales nearly doubled in July, as did the number of US merchants transacting on the platform. The broker upgrades EPS forecasts 8% and 34% for FY19 and FY20. Target price jumps to $21.65.

ALUMINA LIMITED (AWC) was upgraded to Neutral from Sell by UBS. B/H/S: 4/2/0. Alumina’s result and dividend appear to have fallen slightly short of UBS, albeit a 77% increase in earnings reflects strong alumina prices and the best margins since before the GFC, according to the CEO. The company’s capital management policy implies double-digit dividend yields that should support the share price. Target rises to $2.70 from $2.45.

COCA-COLA AMATIL LIMITED (CCL) was upgraded to Equal-weight from Underweight by Morgan Stanley. B/H/S: 0/4/3. First half earnings for Australian beverages were better than Morgan Stanley expected. The broker believes the valuation, relative to the ASX industrials, remains reasonable albeit expensive on an absolute basis. The broker believes the company’s brand leadership and new products have enabled the business to navigate the container deposit scheme impact better than previously expected. Target is raised to $9.60 from $8.00. Cautious industry view.

See also CCL downgrade.

NINE ENTERTAINMENT CO. HOLDINGS LIMITED (NEC) was upgraded to Buy from Neutral by UBS. B/H/S: 3/1/1. Nine’s result was in line with guidance but slightly below UBS. The broker believes management’s assumptions are undemanding, with 1% metro TV market growth and -2-3% in TV cost reductions, implying 39% market share. But before long the market’s focus will switch to the merger with Fairfax. UBS has not yet factored this in but expects upside from synergies, Stan consolidation and asset sales. On the question of whether Nine is a cheap entry point to Domain (DHG), the broker believes the market is unfairly discounting Nine’s TV business to Seven West’s (SWM). Target rises to $2.60 from $2.40.

SOUTH32 LIMITED (S32) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 3/4/0. FY18 numbers slightly beat Credit Suisse estimates. The broker notes multiple potential upside catalysts as well as a more favourable commodity suite versus the major miners. The broker believes opportunities in Illawarra and South Africa, and the evolution of Arizona/Eagle Downs, should be more than sufficient to maintain investor interest. Target is raised to $4.10 from $3.95.

WESTERN AREAS NL (WSA) was upgraded to Buy from Hold by Ord Minnett. B/H/S: 4/2/1. Underlying, Western Areas’ FY18 result fell short by some -4% on lower than expected revenues. On reported numbers, net profits came out well short; $12m versus $17m expected. FY19 guidance is a disappointment also. But Ord Minnett remains hopeful that the Odysseus definitive feasibility study, to be released in September, can turn things around for the share price, and has on this premise upgraded to Speculative Buy from Hold. The target price lost 5% to $3.60.

In the not-so-good books

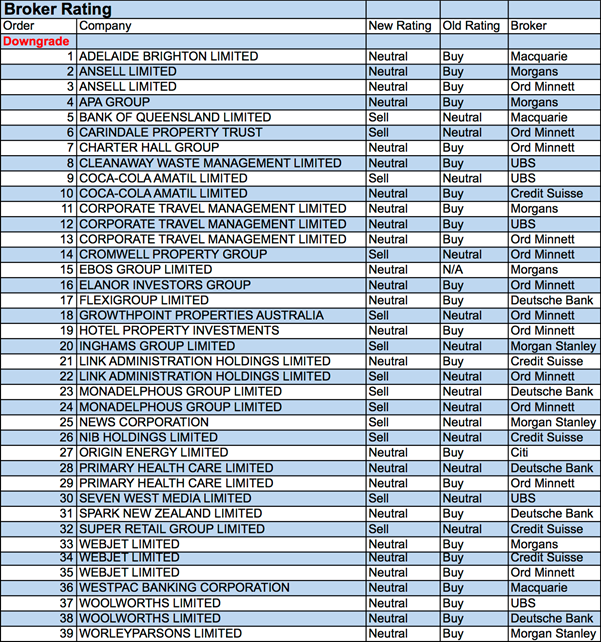

ANSELL LIMITED (ANN) was downgraded to Hold from Add by Morgans and to Hold from Accumulate by Ord Minnett. B/H/S: 1/6/1. Ansell’s result was broadly in line with Morgans but required lower tax and interest and a buyback to support solid organic sales growth, offset by flat margins due to raw material headwinds. Target falls to $25.16 from $26.30. Ansell broadly delivered on Ord Minnett’s FY18 expectations but organic growth has slowed and most of the 10% rise in H2 operating earnings was due to cost savings from restructuring. Management has guided to a much weaker outlook in FY19 than the broker had anticipated, due mainly to rising input costs, leading Ord Minnett to cut FY19 forecasts by 10%. Target is reduced to $24.70 from $29.75.

[2]

[2]

COCA-COLA AMATIL LIMITED (CCL) was downgraded to Sell from Neutral by UBS and to Neutral from Outperform by Credit Suisse. B/H/S: 0/4/3. Corporate costs, losses for SPC and weakness in Indonesia meant Coca-Cola Amatil’s result fell short of UBS. The Australian division beat the broker by 3% but was still down 9% year on year due to heightened investment, which will continue to year’s end. Target falls to $8.30 from $8.40. Credit Suisse believes the stock is now priced correctly for what is on offer, which is low single-digit growth in earnings per share. Target is $9.80.

See also CCL upgrade.

CHARTER HALL GROUP (CHC) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 2/2/1. Higher corporate costs have caused Charter Hall’s FY18 operating result to miss Ord Minnett’s expectation by some -3%. The analysts note the shares have significantly outperformed over the year past as investors switched their preference to office and industrial assets, which represent 60% of Assets under Management at Charter Hall. Post share price outperformance, Ord Minnett downgrades to Hold from Accumulate. Target price unchanged at $6.90.

CORPORATE TRAVEL MANAGEMENT LIMITED (CTD) was downgraded to Hold from Add by Morgans, to Neutral from Buy by UBS and to Hold from Buy by Ord Minnett. B/H/S: 1/4/0. Morgans was impressed with FY18 earnings, noting second half growth of 21% is significant for a company of this size. All regions were largely in line with forecasts. FY19 guidance is for EBITDA of $144-150m, up 15-20%.

Morgans downgrades to Hold from Add because of the strong appreciation in the share price. Target is reduced to $32.00 from $32.25. Corporate Travel’s result was hard to fault, UBS suggests, featuring impressive organic growth of 19%. But it’s all already in the price. Target rises to $32.20 from $27.50. Ord Minnett also downgrades on valuation grounds. Target rises to $30.30 from $24.36.

SUPER RETAIL GROUP LIMITED (SUL) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 2/5/1. Super Retail’s result outperformed low expectations, Credit Suisse notes, but it required outperformance from Auto and Macpac to offset ongoing weakness in BCF and Sport. Guidance to 11 new Auto stores was a surprise. The broker is perplexed as to why inventory levels for BCF and Auto were so high at year-end. The broker is also uneasy about a management reward structure based on normalised profit, which encourages risk taking without an offset for weakness accountability. Credit Suisse lifts its target to $8.39 from $8.36.

SEVEN WEST MEDIA LIMITED (SWM) was downgraded to Sell from Neutral by UBS. B/H/S: 0/3/3. FY18 results were at the top end of guidance. Relative to UBS forecasts, FY19 cost reduction guidance of $10-20m is below previous estimates. The broker remains positive about the earnings momentum and the ability to grow share into FY19. However, with the stock re-rating above valuation the broker downgrades to Sell from Neutral. Target is $0.85.

WEBJET LIMITED (WEB) was downgraded to Hold from Add by Morgans, to Hold from Buy by Ord Minnett, and to Neutral from Outperform by Credit Suisse. B/H/S: 1/4/0. Webjet’s FY18 result outpaced consensus and Morgans, and was struck on strong revenue, margins and operating cash flow. Morgans says the performance makes Webjet the fastest growing B2B player in the world. For now, Morgans upgrades forecasts across FY19 to FY21 and increases the target price to $17.15 from $13.75. Rating is downgraded to Hold from Add, after strong share price appreciation. Clearly, it was a “stand-out result”, the analysts at Ord Minnett assert. Target price moves up to $17.46 from $14.00, but the rating has been pulled back to Hold from Buy following a stellar rally in the share price after the release of FY18 financials. Credit Suisse also downgrades on valuation grounds. Its target is raised to $16.00 from $13.65.

WORLEYPARSONS LIMITED (WOR) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 3/3/1. Reported FY18 financials were in line with expectations. Morgan Stanley observes the stock has regained its sector premium in recent times and thinks it’s now most appropriate to downgrade to Equal-weight from Overweight. WorleyParsons is performing well, conclude the analysts, adding the cycle looks good, but it will take time for earnings to grow significantly. Price target lifts to $20.13 from $18.70.

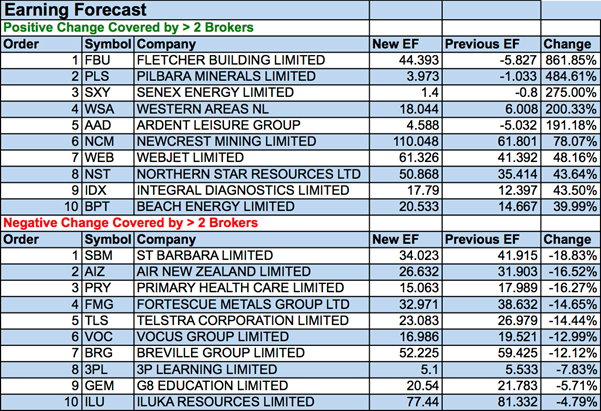

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

[3]

[3]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.