Stockbroking analysts sent the local share market into the new financial year with positive momentum. For the final week of June, ending on Friday the 29th, FNArena registered 11 upgrades versus nine downgrades.

Confession season is in full swing in Australia, with Telstra and Ramsay Health Care thus far having proven there is no natural limit to negative news. With less than one full month to go before the August reporting season, investors in Australia will increasingly focus their radar on what might unfold next. This might translate into low volumes and overall reticence towards taking risk.

In the good books

AURIZON HOLDINGS LIMITED (AZJ) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 3/2/2. The investor briefing confirmed FY18 guidance and noted the various challenges facing the business in FY19 as well as highlighting further opportunities for efficiencies. Deutsche Bank upgrades fourth quarter coal volumes and adjusts longer-term expectations based on the latest Wood McKenzie production forecasts. Rating is upgraded to Hold from Sell and the target to $4.25 from $4.10.

[1]

[1]

COLLINS FOODS LIMITED (CKF) was upgraded to Buy from Hold by Deutsche Bank. B/H/S: 3/0/0. The FY18 result underwhelmed Deutsche Bank as margins were disappointing and comparables soft. Margin weakness in Europe reflected the costs associated with establishing a presence in Germany and the Netherlands, although Deutsche Bank still views this expansion favourably as a long-term strategy. Meanwhile, recent trading in Australia has been more positive and FY18 will present an easier comparable base. Target is increased to $6.30 from $5.50.

CSR LIMITED (CSR) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 1/4/1. At the AGM, management has provided additional guidance for net profit of $176-204 million. Recent strength in building approvals is expected to support volumes in FY19. Deutsche Bank notes the performance of Viridian continues to improve, albeit from a small base. Target is raised to $4.88 from $4.68.

ERM POWER LIMITED (EPW) was upgraded to Neutral from Underperform by Macquarie. B/H/S: 0/3/0. Renewable energy certificate prices are falling, and every -$10 drop could add $19 pre-tax for ERM, Macquarie notes, although the company’s hedge position is not known. Addressing the US market remains a major catalyst, but downside risk is priced in, Macquarie believes. Upgrade to Neutral from Underperform. Target rises to $1.44 from $1.39.

NORTHERN STAR RESOURCES LTD (NST) was upgraded to Buy from Sell by UBS. B/H/S: 1/3/3. UBS takes a fresh look at Northern Star Resources with a new lead analyst. The broker believes the company’s production aspirations are conservative. Modelled production is lifted to 692,000 ozs for FY19 and 697,000 ozs for FY20. Rating is upgraded to Buy from Sell, driven by growth in production, earnings and cash flow. Target is raised to $7.50 from $6.06.

QBE INSURANCE GROUP LIMITED (QBE) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 4/4/0. Deutsche Bank upgrades QBE to Hold from Sell following a period of weakness. The broker’s concerns over the operating complexity and the underwhelming returns remain intact. Since the downgrade in August last year the company has exited its Latin American assets, replaced its CEO and CFO and remains in the process of simplifying its operations, the broker notes. Target is $10.

WESTERN AREAS NL (WSA) was upgraded to Neutral from Sell by UBS. B/H/S: 2/1/3. UBS has increased nickel price forecasts by 12% in 2018 and 6% in 2019, leading to an 82% FY19 forecast earnings upgrade and 19% FY20 upgrade for Western Areas. The broker notes the planned Odysseus project should see first production at a time global EV demand has led to higher nickel prices.UBS upgrades to Neutral from Sell. The broker would be more positive but the share price is overvaluing either the nickel price forecast or Odysseus risked valuation or both, UBS believes. Target rises to $3.50 from $3.02.

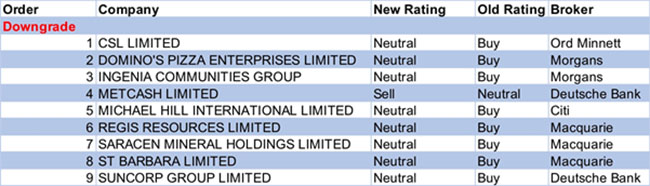

In the not-so-good books

CSL LIMITED (CSL) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 4/4/0. Ord Minnett believes the risk/reward profile has become less compelling and downgrades to Hold from Accumulate. That said, the broker remains confident that the company will have another year of earnings growth in the mid teens, supported by therapies such as Idelvion, Haegarda and Hizentra. Target is unchanged at $195.

[2]

[2]

MICHAEL HILL INTERNATIONAL LIMITED (MHJ) was downgraded to Neutral from Buy by Citi. B/H/S: 2/2/0. Citi analysts have changed their view about Michael Hill having less exposure to a troubled household spending budget, which earlier underpinned the Buy rating for the stock. The shares look cheaply priced, but Citi nevertheless downgrades to Neutral from Buy. Price target dives to $1 from $1.43 on reduced forecasts. The broker questions the limited growth options.

SUNCORP GROUP LIMITED (SUN) was downgraded to Hold from Buy by Deutsche Bank. B/H/S: 4/3/1. The stock has recently traded above Deutsche Bank’s fundamental valuation and, despite the short-term upside from the potential sale of life assets, the rating is downgraded to Hold from Buy. Target is $14.50.

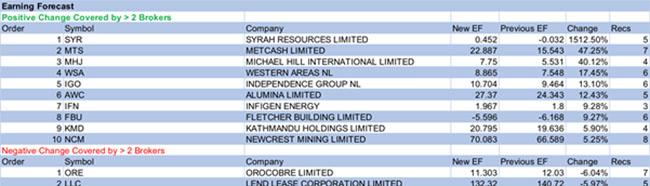

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

[3]

[3]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.