The Australian share market has posted only small net gains so far year-to-date (including dividends), but June might well add some more, assuming global sentiment doesn’t sour in the remaining twelve days.

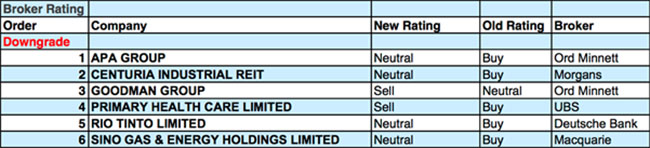

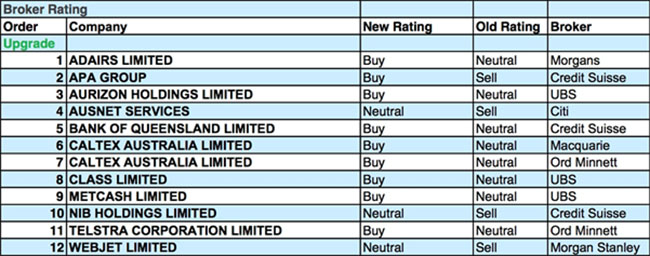

Stockbroking analysts for their part are trying their best to keep sentiment positive. For the week ending Friday, 15th June 2018, FNArena counted twelve upgrades for individual ASX-listed stocks against six downgrades. Caltex Australia received two upgrades during the week and both went to Buy.

Other stocks receiving upgrades include Telstra (!), Bank of Queensland, Metcash and Webjet. Only two of the six downgrades moved to Sell with Primary Health Care and Goodman Group the recipients.

In the good books

APA GROUP (APA) was upgraded to Outperform from Underperform by Credit Suisse. B/H/S: 3/3/1. Following the news that CKI consortium is offering $11 per share to shareholders, Credit Suisse has double-whammy upgraded to Outperform from Underperform. The analysts make it clear they think the offer is regarded as “attractive” given their view that new arbitration rules “dramatically” reduce the economic life of APA’s assets. Within the Australian context, the analysts point out CKI has a track record of paying what others won’t. FIRB approval remains key. Target price lifts to $11 (was $7.45 pre-bid).

See also APA downgrade.

[1]

[1]

AUSNET SERVICES (AST) was upgraded to Neutral from Sell by Citi. B/H/S: 2/4/1. Following the recent underperformance of the share price Citi upgrades to Neutral from Sell and considers the stock fairly valued. The broker also updates its model for the FY18 results, which slightly missed expectations. The broker continues to prefer Spark Infrastructure (SKI) in the sector. Target is $1.54.

AURIZON HOLDINGS LIMITED (AZJ) was upgraded to Buy from Neutral by UBS. B/H/S: 3/1/3. UBS believes heated and protracted negotiations over the draft decision by the Queensland regulator have skewed sentiment to an extreme negative such that an improvement is now more likely. The broker suggests the stock is approaching a realistic floor of $3.75 based on the network being worth its regulated asset base, less debt. Target is reduced to $4.60 from $4.90.

BANK OF QUEENSLAND LIMITED (BOQ) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 2/2/2. Credit Suisse believes the stock is now trading below fair value and represents a good entry point. While acknowledging a challenging macro backdrop for the sector the broker calculates Bank of Queensland is currently sitting near the trough in valuation across most metrics. Target is steady at $11.40.

CALTEX AUSTRALIA LIMITED (CTX) was upgraded to Outperform from Neutral by Macquarie and to Buy from Hold by Ord Minnett. B/H/S: 5/1/1. Caltex has provided first half profit guidance that is in line with Macquarie’s expectations. The broker observes the core business is defensive and earnings growth is expected. Future drivers are the asset review and convenience strategy. The broker increases the target to $37.00 from $36.60. The company’s net profit guidance for the first half of $295-315 million is ahead of Ord Minnett’s forecasts, as refining has fallen less than expected. The broker raises the target to $35 from $34 because of earnings revisions, confidence in refiner margins and the positive changes emerging in the asset portfolio.

METCASH LIMITED (MTS) was upgraded to Buy from Neutral by UBS. B/H/S: 4/2/1. UBS upgrades to Buy from Neutral, believing the company’s FY19 earnings multiple for the food and grocery division is pricing in further contract losses. The broker lifts FY19-21 forecasts by 1% to reflect stronger hardware earnings. Target is raised to $3.00 from $2.95.

NIB HOLDINGS LIMITED (NHF) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 0/6/2. Credit Suisse lowers FY19 net profit estimates by 0.1% on the assumption that premium rate increases will be less than 3%. In FY20 and the outer years the broker allows for a 2% premium rate increase and minor margin contraction. While the broker struggles to be positive on the stock, the share price has moved back to around fair value. Target is reduced to $5.35 from $5.65.

TELSTRA CORPORATION LIMITED (TLS) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 5/1/2. Ord Minnett expects the company to announce an additional $500 million – $1 billion of cost savings and new product bundling initiatives at its strategy briefing on June 20. There is also the chance of a game-changing announcement such as a structural separation. The broker upgrades to Accumulate from Hold. Target is $3.30.

WEBJET LIMITED (WEB) was upgraded to Equal-weight from Underweight by Morgan Stanley. B/H/S: 4/1/0. As global hotel trading has provided strong tailwinds to the company’s key B2B exposures, Morgan Stanley expects the market will give a free pass on key qualitative issues such as soft cash conversion and higher capital expenditure. Target is raised to $12.60 from $10.30. Industry View is In-Line.

In the not-so-good books

APA GROUP (APA) Downgrade to Hold from Buy by Ord Minnett. B/H/S: 3/3/1. After further review of the bid by CK Infrastructure for APA Group, Ord Minnett has downgraded to Hold from Buy. The main challenge in getting a deal done, the broker suggests, is approval from the FIRB, even though the stock factors in a 58% likelihood of success. The broker raises the target to $11.00 from $9.55.

See also APA upgrade.

[2]

[2]

GOODMAN GROUP (GMG) was downgrades to Lighten from Hold by Ord Minnett. B/H/S: 3/3/0. Ord Minnett believes the business is in great shape but the stock is expensive versus history and its peers. The broker is also somewhat concerned about the quality of earnings growth. Target is raised to $8.40 from $8.10.

PRIMARY HEALTH CARE LIMITED (PRY) was downgrades to Sell from Buy by UBS. B/H/S: 1/1/5. UBS changes lead analyst coverage for the stock and remodels earnings drivers. FY19-20 forecasts decline by 8-9% versus previous estimates. Target reduces to $3.50 from $4.00. The broker does not believe the current share price is factoring in the earnings risk as several factors could have a negative impact on FY19.

RIO TINTO LIMITED (RIO) was downgraded to Hold from Buy by Deutsche Bank. B/H/S: 7/1/0. While believing some of the bear scenarios regarding rapidly rising scrap consumption are premature, Deutsche Bank expects Chinese demand for iron ore to peak around 2020 and limit the growth potential for the major producers. The broker reduces assumptions for Rio Tinto’s iron ore production from 2021. The stock has re-rated versus its peers following a successful strategy of asset sales, de-leveraging and high cash returns. Following this significant rebound the broker downgrades to Hold from Buy. Target is steady at $89.

Earnings forecast

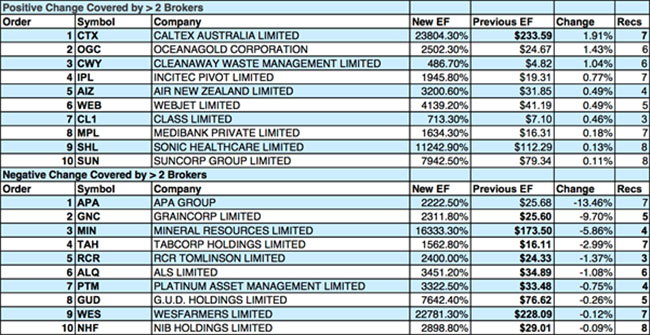

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

[3]

[3]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.