I am going to stick my neck out and say that the banks are a buy! Given that there is so much negativity about the major banks, this feels like something Sir Humphrey Appleby of Yes Minister fame would have labelled a “courageous call”.

Before mounting the case for the major banks, I will start with why they have been poor performers in 2018.

The backdrop

Firstly, the Royal Commission, which by revealing some dreadful practices and systematic bad behaviour, has shocked the community. I, like some others in the financial community, underestimated the extent of the practices and the impact the Commission would have on public opinion and also bank share prices.

The penultimate round of public hearings gets under way today. Scheduled to appear over the next fortnight include representatives from AMP, Suncorp and CommInsure (owned by the CBA). The final round of hearings (if the Commission is not extended) is scheduled for late November, when it will examine policy questions.

Putting the “shock value” to one side, the key issue to consider about the Royal Commission is the likely nature of the recommendations it will make to the Government, and the impacts these could have on the banking industry in the medium term. The areas the Commission may seek to address include: an end to the vertical integration of wealth management business (product manufacturing, investment management, distribution and advice); expansion of “responsible lending” rules to small business, as well as toughening these provisions for consumers; the end of conflicted remuneration arrangements; and changing the commission arrangements on home loans.

But these moves have been widely telegraphed and the banks are already taking action. For example, each of the majors has made moves to exit some, or all, of their wealth management businesses. Westpac possibly sees this as a differentiator, but it has sold off its investment management business (Pendal) and is rumoured to be considering an exit of its financial planning arms.

If the Commission recommends criminal charges against banks or bank executives, or widespread civil actions to penalise and compensate, this could unsettle markets.

However, it is difficult to see what the Commission could recommend that would fundamentally diminish the competitive position of the major banks. While all the bad news may not be out yet, my sense is that “Royal Commission risk” has bottomed.

Other factors

The other factors that have impacted the performance of the banks in 2018 are:

- Revenue growth is anaemic – at best low single digits. Overall credit growth has slipped below 5%, with housing credit growth down to 5.5%. Further, the major banks are losing share to non-bank participants, as APRA’s toughened regulatory stance (particularly in regard to investor lending and interest only loans) bites;

- Interest margins are under pressure as the cost of short-term funds in the wholesale markets (in particular, the relationship between the 90-day bank bill rate and the overnight cash rate) moves higher;

- Fears that a major downturn in the housing market could pressure bank balance sheets and increase losses;

- Increasing compliance costs;

- Suggestions that the investment into Fintech style initiatives, supported by reforms such as Open Banking (the exchange of customer data between banks), will, in the medium term, materially disrupt the competitive position of the major banks; and

- Selling by SMSFs and others as fears widen that Bill Shorten will be Australia’s 31st Prime Minister, and the ALP will proceed with its plan to abolish the refunding in cash of excess imputation credits.

The case for

The case for is relatively straightforward. Firstly, the major banks still enjoy a fantastic oligopoly with immense pricing power (witness the “out of cycle” rate increase to home loan rates by CBA, ANZ and Westpac over the last two weeks).

While there is a slow drift in customers from the major banks to the minor banks/“non-banks”, it is tiny. Despite consumers saying that “they want to change banks”, their actions don’t match. All the evidence points to an incredible degree of inertia.

Capital ratios are sound. With the possible exception of the NAB, the majors are on track to reach APRA’s new definition of “unquestionably strong”. This means no dilutive capital raisings, and again with the possible exception of the NAB, dividends are secure.

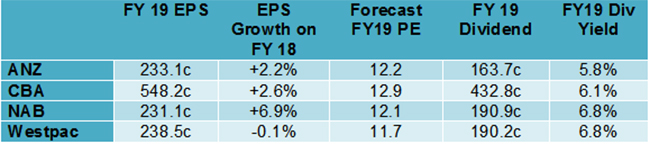

Banks are cheap. They are trading on a forecast multiple of FY19 earnings of between 11.7 and 12.9 times (see table below based on broker consensus estimates, source FN Arena). And notwithstanding the challenges about growing revenue and funding pressures, earnings per share growth is occurring.

Forecast Multiples, EPS Growth and Dividend Yields

[1]

[1]Source: FN Arena 7/9/18

Bad debts remain low, and the two most likely triggers, higher interest rates or higher unemployment, aren’t on the cards. The opportunity to radically take out cost by cutting branch networks, digitising processes and reducing head office bureaucracies remains, although each of the major banks is now acting to cut costs.

Finally, dividend yields are super attractive (forecast 5.8% for the ANZ to 6.8% for Westpac). And even in a Bill Shorten world, where excess franking credits are not refundable, a 6.8% yield for an SMSF in pension phase is still a lot more attractive than a term deposit rate of 2.5%!

Which bank?

The obvious question then becomes “which bank?” The answer is that it probably doesn’t matter that much as they are essentially pursuing the same strategies and the differences from one bank to the next are at the margin.

But before coming back to this question, let’s look at how they have done this year and what the major brokers have to say.

The table below shows the performances of the major banks in 2018. Only ANZ has delivered a positive return to shareholders of 1.6%. I put this down to two factors – it is the most focussed (and advanced) in its cost out initiatives, and possibly, carries the least “Royal Commission” risk.

Major Banks Performance in 2018

[2]

[2]

Westpac is the weakest performer (loss of 8.3%), with much of the downside coming recently following the revelation of funding pressures. It is also the “most exposed” in terms of the changes with “interest only” home loans.

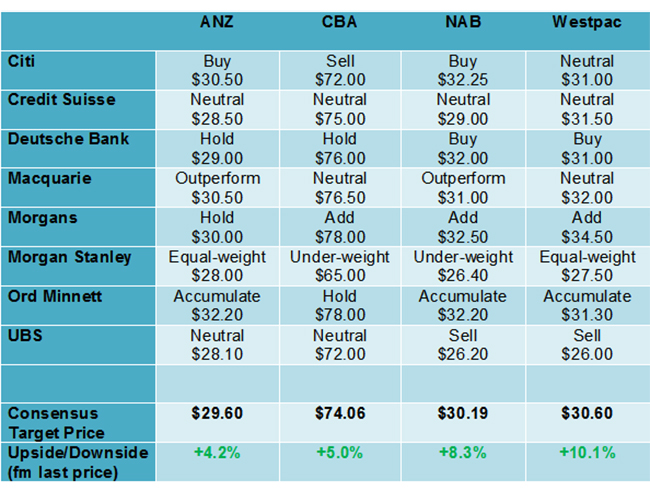

Looking ahead, the major brokers are largely neutral about the prospects of the major banks. The following table shows the major brokers recommendations and target prices for the banks.

In summary:

- There is no standout “preferred” bank;

- They see upside (limited) for each of the major banks. Westpac has the most upside of 10.1% (trading at $27.80 versus a consensus target price of $30.60), ANZ has the least upside of 4.2%;

- NAB has the most “buy” recommendations (four “buy”, two “neutral”, and two “sell”).

Broker Ratings – Major Banks (Recommendation and Target Price)

[3]

[3]Source: FN Arena 7/9/18

I have been on the ANZ bandwagon this year and in this respect, been proven to be right. However, it is now the second most expensive on forward multiple, and Westpac is (unusually) the cheapest. As the differences between the banks are so small, on value grounds, my vote goes to Westpac.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.