Aristocrat Leisure (ALL) remains a core holding in the AIM Global High Conviction Fund. The company is an ASX listed global leader in its sector, and its dominance over its sector continues to expand.

ALL is a structural growth stock. This was again reaffirmed last week when the company again upgraded earnings guidance for 2017 at their Annual General Meeting. ALL stock responded positively to the AGM upgrade, moving to fresh record highs.

My view is that there’s more to come from ALL and the upgraded guidance range will be exceeded when full year results are released later in 2017.

Every piece of direct industry feedback suggests ALL continues to win market share in both the domestic and North American poker machine segment. They have the best products and service, which is translating to profitable market share gains and margin expansion.

ALL confirmed a strong start to 2017. ALL stated “the first 4 four months of trading have been strong”. That is unambiguous guidance.

In terms of physical profit growth guidance, ALL upgraded their 2017 guidance to “+20% to +30% at the NPATA level. The mid-point of this new guidance exceeds the previous Bloomberg consensus estimate that had expectations of +20% NPATA growth. The new mid-point of guidance implies FY17 NPATA of $498m.

As you would expect, the analyst community upgraded their forecasts to the mid-point of the new guidance range. That will prove too conservative and my view is ALL will deliver a FY17 result above the top end of the new guidance range. I would expect +31% NPATA growth from ALL in FY17, or more, which will see further upgrades to consensus numbers later this year.

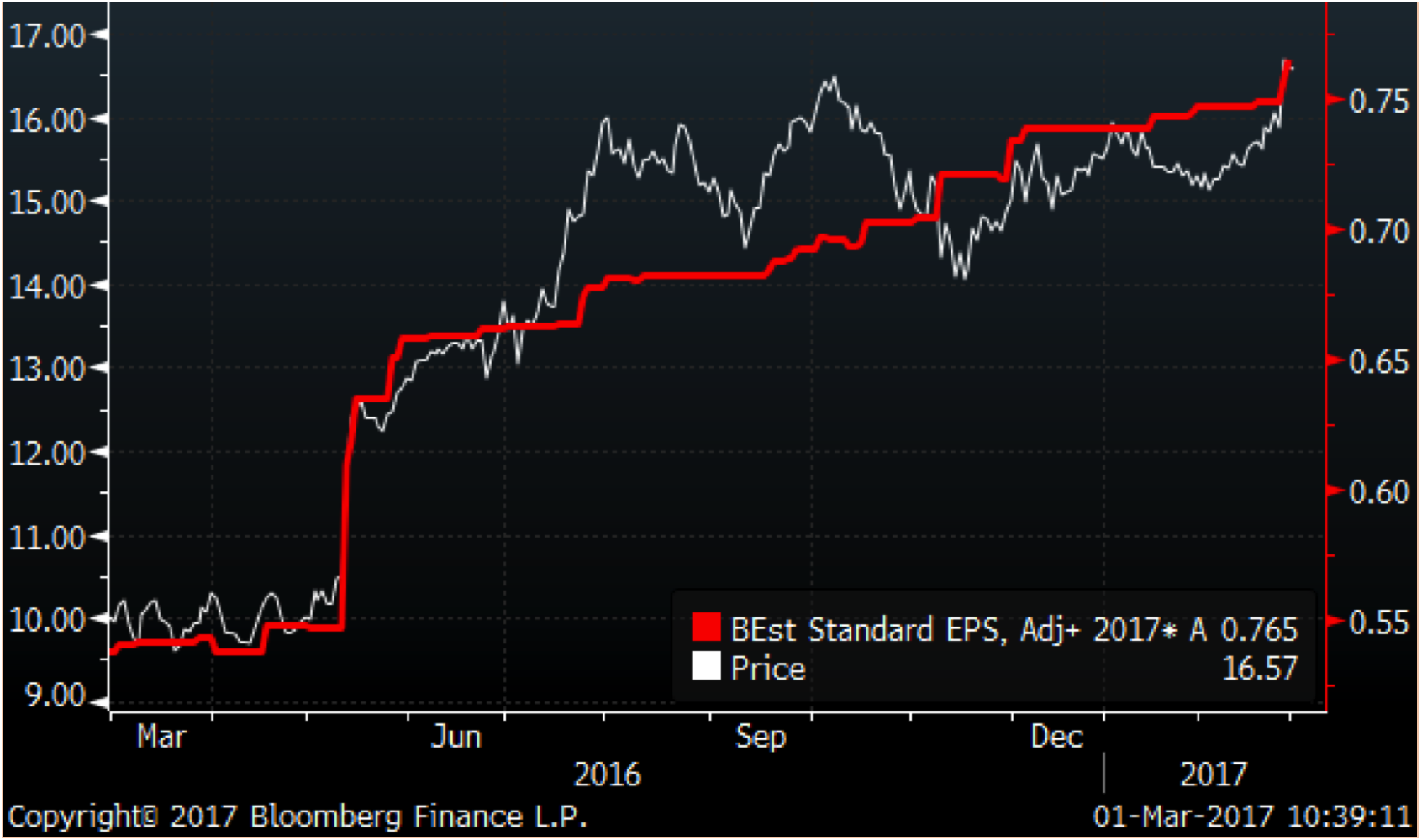

Below is the FY17 consensus ALL EPS forecast (red) vs. the Aristocrat (ALL) share price. You can see the share price broadly tracks consensus earnings upgrades, of which I believe there are more to come.

[1]

[1]Why I think the analysts are too conservative is simply based on the view that this is unusual for ALL to give full year earnings guidance at their AGM just four months into their financial year. They DID NOT do that last year and to me it suggests they have great confidence and visibility in their revenue streams.

I had been hopeful that ALL’s AGM would be a positive stock price catalyst. That certainly was the case but even I was surprised (positively) by the scale of the upgrades and the confidence that management displayed.

This is particularly important as ALL is in the middle of a CEO’s succession that made some people previously nervous. Long standing CEO Jamie Odell is handing over to Trevor Coker in what appears so far to be a seamless transfer of leadership. In fact, it has been a textbook execution of succession so far and another reason I see ALL’s P/E expanding in the weeks and months ahead.

The confirmation of strong earnings at the start of Mr Croker’s tenure (March 17th) confirms there has been no loss of momentum in the business, in fact, the business has gained momentum during the CEO transition period. This is very good news for Mr Croker and means he takes over a business travelling very strongly.

It would appear momentum in ALL’s North American business is driving the earnings upgrades. While there was no detail from ALL and what drove the guidance upgrade, it seems fair to conclude that ongoing momentum in North American participation and shipments (40% of profits) are the drivers.

This is where the analyst community upgraded their numbers after the AGM guidance upgrade, yet I still feel those revised up forecasts will prove conservative.

For example, Citi, who have the no.1 rated gaming analyst now forecasts +27% NPATA growth from ALL in 2017, driven by +23% (yoy) growth in North American Class III Participation net installed base (3,200 units, up from 2,900 units) as well as +5% (yoy) growth in average fee per unit to US$59.50 per day.

They also expect +6% (yoy) growth in net installs of VGT (1,300 units) and +5% (yoy) growth in average daily fee per unit to US$45.30 per day.

Both these events lead to margin expansion, which to 50% and 70% for the respective North American businesses. Volume growth +margin growth = earnings growth.

ALL is now generating 65% of revenue from North America. It is therefore encouraging to see the new CEO will be based in Las Vegas. Similarly, three non-executive Directors also live there. I think both of those are important points.

It is important because ALL’s growth has been driven by US acquisitions, most notably the transformational $1.4b acquisition of Video Gaming Technologies (VGT), the make of bingo-style class II gaming machines, in 2014.

That VGT acquisition played a key role in increasing the proportion of ALL’s recurring revenue streams. ALL now generates 55% of revenue from recurring revenue streams, which is one reason I believe ALL deserves a P/E premium to the highly cyclical ASX200.

The other great organic success for ALL has been the Lightening Link poker machine, now one of the most popular in the world. The game, originally developed to help ALL turn around a slump in business in Queensland, is now the most popular game in North America. It was also just launched in Asia.

You would think with all this good news and momentum, ALL would be a very expensive stock. That is NOT the case and I remain of the view that the world leader in its sector is CHEAP versus its structural growth prospects. The P/E and PEG ratios have actually become CHEAPER as the earnings forecasts have moved higher, meaning this stock is far from priced as a “jackpot”.

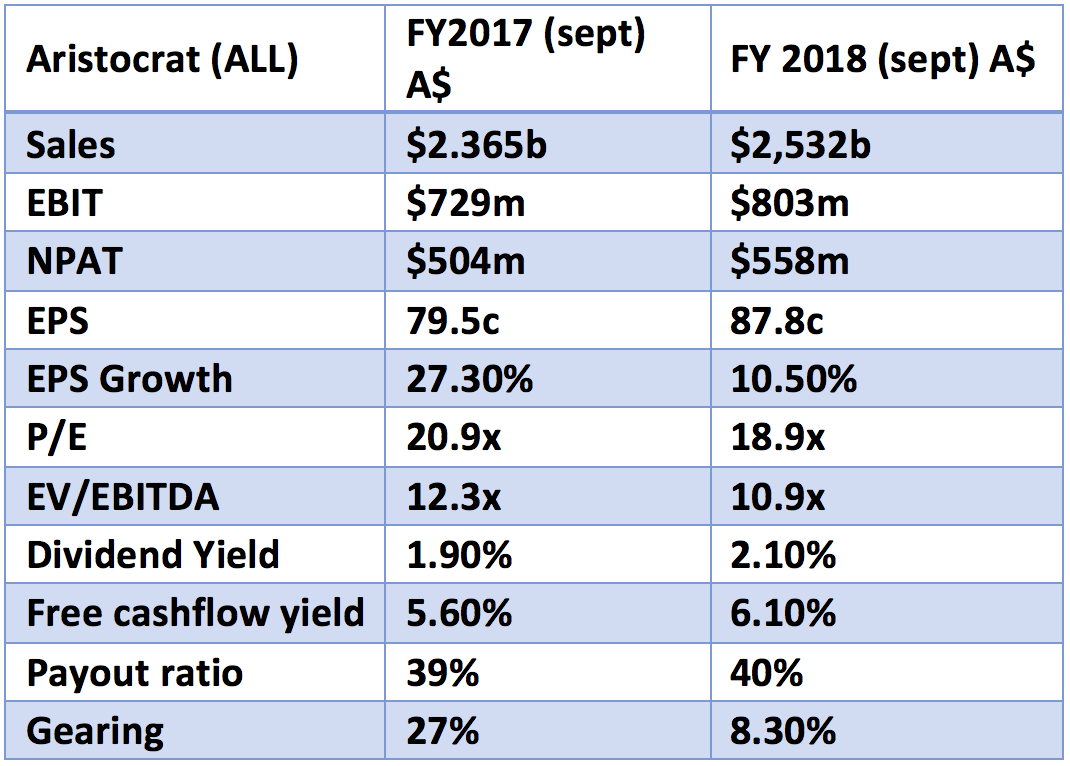

Below are Citi’s forecasts for 2017 and 2018. They are higher than consensus but lower than what I think will be delivered.

[2]

[2]ALL exceeds every metric I look for in a stock, but the key attraction is the FY17 Price to Growth Ratio (PEG) of just .76x. You can buy the world leader in the sector at just .76x PEG ratio. That to me is cheap and my personal view is ALL shares will head towards $19.00 this year, delivering investors a total return of +20% from these levels ($16.60).

ALL remains a high conviction investment. I encourage you to consider an investment in ALL, you haven’t “missed it”.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.