Today I want to introduce you to an ASX listed small cap growth stock that exceeds all the attributes I look for in an investment. It also has the added attraction of a high fully franked (growing) dividend yield.

The stock is IVE Group (ASX Code: IGL), a $300m market cap stock that I believe has the potential to deliver solid total returns over the years ahead.

IVE is a vertically integrated marketing services and print communications provider. IVE enables its customers to communicate more effective with their customers by creating, managing, producing and distributing content across multiple channels.

I’d be pretty sure most of you have never heard of IVE but I’d also be pretty sure you’ve read one of the catalogues they have printed for major retailers.

Catalogues remain a very effective form of advertising for a wide variety of consumer-facing companies. Due to industry consolidation, two players now control the vast bulk of the catalogue market in Australia. However, the equity market attributes a very low P/E to this sector because they are unsure whether it will succumb to technological change (digital mediums).

After meeting with the highly impressive IVE management team earlier this week, I think “IVE will THRIVE”. This is a genuine growth stock priced like the industry won’t be around in five years. IVE is expanding and enhancing its product offering to embrace digital medium as well, and I feel this stock is genuinely mispriced (too cheap).

The marketing services and print communications industry is dynamic and constantly evolving. IVE has responded to its customers’ needs via investing and expansion of its product and service offering. Growth has been organic and acquired. IVE holds leading positions across multiple industry sectors.

One thing I always look for when considering investing in a small cap stock is “who are their customers?” and secondly “how dependent are they on one key customer?”

Analysis of IVE’s customer base reveals an absolutely blue chip list of top 100 Australian and multi-national major companies. IVE has successfully rolled over a number of key contracts across the group: Commonwealth Bank, Westpac, Travelcorp, Australian Electoral Commission, Fairfax, Glaxo Smith Kline, Bauer Media, Next Media and Flight Centre. The company has also secured major new contract wins from Coles Supermarkets, L’Oreal, Diageo, BP, Blackmores, Norwegian Cruise Lines, Globus, Helloworld, Nestle, Suncorp, Foxtel, Just Group, AXA and Treasury Wine Estates.

Alongside that, IVE’s biggest single customer only accounts for 6% of group revenue. The top 20 customers comprise 35% of IVE’s total revenue. That is solid diversity and that diversity continues to increase via contract wins.

In total, IVE has transacted with over 2,200 customers, demonstrating the Groups stability and scalability as a reliable partner in the marketing services and print communications sector.

IVE has maintained a disciplined acquisition strategy, with five businesses acquired throughout the 1H of FY 2017. The 1H saw the successful integration of three acquisitions into existing businesses, building on their strong operational footprint and market position. The Mailing House, Display Bay and R25 are all operating in line with business cases in respect to key metrics and synergies.

IVE’s biggest acquisition to date was the purchase of Franklin Web and AIW Printing just before the end of last year. While only early days, the company is confident that the rationale for this major acquisition is correct and they provided an update since the acquisition at the interim result.

Customers: A very positive response with all customers of both Franklin Web and AIW retained and keen to explore the broader IVE offer. Significant new business win, securing the Coles Supermarkets’ catalogue printing contract.

People: All key staff retained

Integration: The integration of AIW and Franklin is well progressed and in line with the business plan.

Synergies: The operational synergies as outlined in the capital raising presentation in December have now been validated. IVE confirmed the synergies will be a minimum of $11.5m per annum.

Capital Expenditure: As a result of securing the Coles contract and to ensure IVE is able to pursue other opportunities, total capital expenditure will be $30m. As a result of the expenditure above, FY18 expenditure will be significantly less than the prior years.

Market update: The ACCC announced on February 17th that it would NOT oppose the merger of ASX listed PMP and IPMG (Independent Print Media Group). The merger once completed will result in two major industry participants in the LFWO (Large Format Web Offset) sector, IVE and PMP/IPMG.

The ACCC approval of the PMP/IPMG deal means we are likely to have two strong rational players in the catalogue segment. In my view, this is an important development in an industry that has previous suffered from bouts of irrational pricing competition.

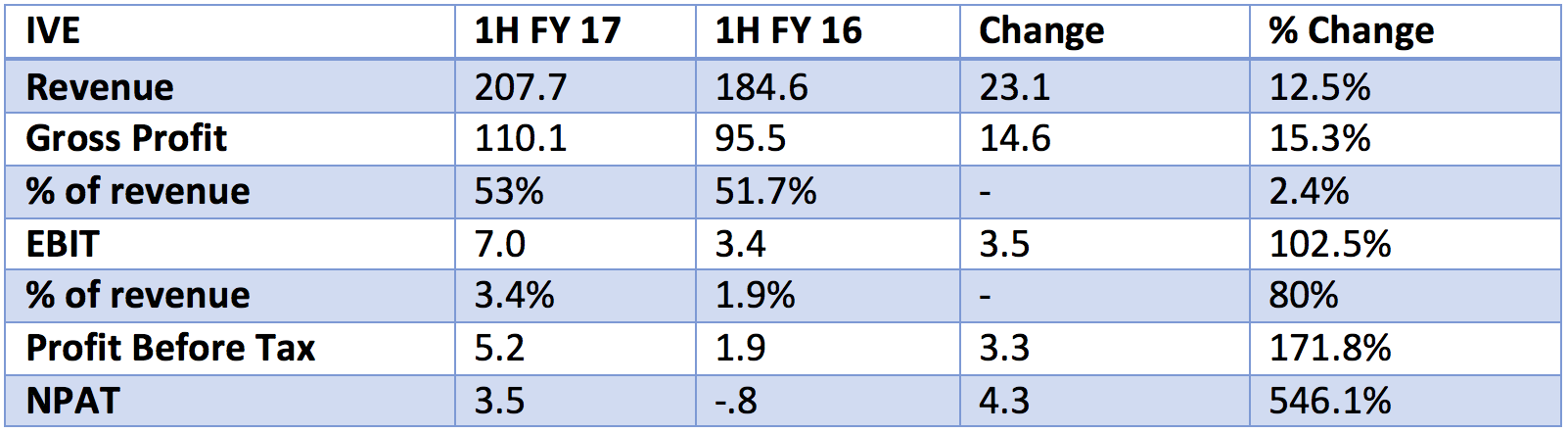

This is good news as IVE already has solid profit momentum in its businesses. The table below summarises year-on-year growth in key IVE metrics.

[1]

[1]IVE gave an upbeat outlook statement about the full year.

- All key components of the AIW and Franklin integration and expansion plan are on track and will be completed in less than 12 months of acquisition.

- Expected synergies validated with a minimum of $11.5m per annum (full run rate).

- EBITDA range of $54m to $57m for FY17.

- Business very well positioned for a strong FY2018.

- Dividend policy unchanged with a payout ratio of 65% to 75% of NPAT.

So what does that all translate to??

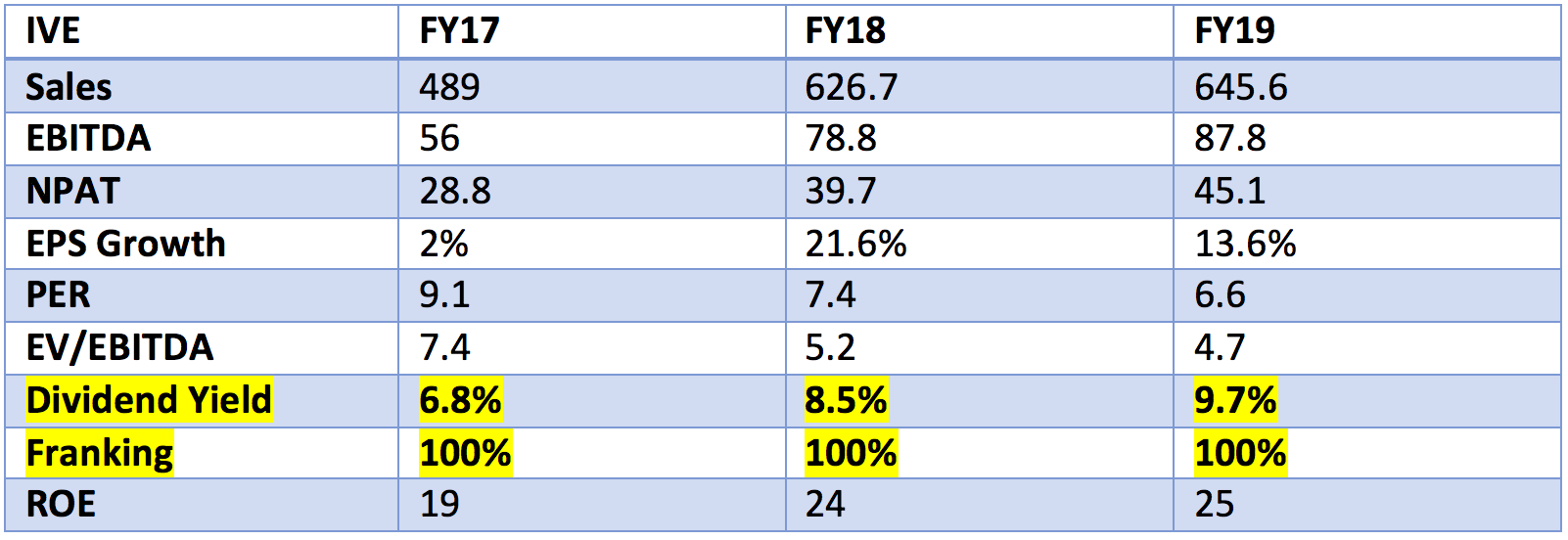

Below is a table containing forward earnings estimates and key ratios for IVE.

[2]

[2]Fy18 is only four months away and that is the year where strong growth kicks in for IVE. On our forecasts, if IVE management delivers to expectations then the stock should grow EPS buy over +20% and the fully franked dividend yield will be 8.5%. All this for a P/E of 7.4x.

Usually high yield = low growth. But here we have high growth and high yield, but the P/E of 7.4x suggests it is unsustainable. We don’t think that is the case and as the market gets more confidence in the strategy and execution, I expect that P/E to rise.

FY18 EPS is forecast at 33.3c. It wouldn’t be a stretch to expect the market to pay 10x for that earnings stream. That sets an 18-month forward price target for IVE of $3.30, vs the current share price of $2.36.

The other interesting aspect is IVE shares are still cum the 6.3c fully franked interim dividend until the 13th of March. That is a nice little bonus to collect for new investors in the stock in the next week.

I believe IVE is a cheap income + capital growth stock and I recently bought the stock for the AIM Global High Conviction Fund. It is a small cap stock and small cap stocks aren’t without risks and volatility.

However, on a prospective FY18 P/E of 7.4x, with prospective earnings growth of +21% and a prospective FY18 dividend yield of 8.5% fully franked, plus still being cum the 6.3c ff 1H Fy17 interim dividend, I think investors are being well compensated to take the risk in IVE shares.

I encourage income and growth investors to consider an investment in IVE at an appropriate size in portfolios.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.