It’s no surprise for you to read that I’d like to say “all’s good” for stock buying right now but it’s not. The Trump trade war, the strong US economy and its implications for inflation, as well as interest rates on top of the debt that bankrolled us out of a potential Great Depression, are all making unbridled positivity impossible.

And the pressure has been particularly piled on overnight, despite a not-so-great jobs report out of the US. When I saw the Dow down over 200 points on bounding out of bed, I thought: “Another good jobs number, which means higher expectations of faster rising interest rates and so stocks down.”

But au contraire!

Jobs came in at 134,000 in September, compared to economists’ forecasts of 185,000. However, the August number was revised up from 201,000 to 270,000! So, over the two months, the average is over 200,000 and unemployment fell to 3.7%, which is the lowest rate since 1969!

So, it’s not “au contraire” but exactly as I thought — the US economy is powering, so the expectations about interest rates rising, and all the worries that go with that, are valid. The big question for all of us is: how long can the drivers of the bull market resist the gravitational pull of stocks in the current setting?

The current belting up of tech or FANG stocks in the USA is because stock markets there have hit all-time highs and this rising rates story has to encourage profit-takers to do exactly that. I don’t think they’ll stay on the sidelines for too long.

There’s 31 days to the mid-term elections — possibly a month of madness and mayhem ahead — and the ultimate polling results there could send stock markets in either direction, with real oomph. Meanwhile, the China trade war will play out over that time in the context of how the US President plans to leverage his America-v-China battle. Did I say madness and mayhem?

Luckily, the US economic and company earnings story should act as a ballast to keep the stock market balanced and on track but the ship called Wall Street is about to encounter some big waves until we see the plain sailing we associate with December.

These great two-month job numbers have to be seen in the context of what the Fed boss, Jerome Powell, said earlier this week, when he suggested there were quite a few rate rises before his interest rate policy was seen as “neutral”.

By the way, this is all because of the good news that the US economy is stronger than doubting Thomas economists were arguing, when they were talking about downward sloping yield curves, and how that kind of thing ran just ahead of a recession. The opposite is happening, so recession looks further away and I’d be more certain of that if I didn’t have to process a trade war scenario.

But it is what it is.

“The labor market is going to keep getting tighter and that will mean higher wages,” said Peter Cardillo, chief market economist at Spartan Capital Securities. “This is going to keep upward pressure on rates and continue to put downward pressure on stocks.” (CNBC) It doesn’t mean the bull market is over, but growth stocks could find it harder to surge and smarties will be chasing value stocks, which should be good for financials, and I’d be happy about that if we didn’t have the Royal Commission fallout and an election to factor into our money-making equation.

To the local stocks story and the S&P/ASX 200 index lost 0.4% over the week, despite positivity creeping in towards the end of the week, partly helped, I suspect, by a weaker dollar.

And if we didn’t have credit crunch stories spooking share players with the effects of the Royal Commission, the ultimate response of the Morrison Government and the alternative threats/promises of the Shorten Opposition, as it jockeys to win the next election, all are no help to bank share prices. So it’s no surprise that the CBA lost 2% for the week, while NAB dropped 2.2% and both Westpac and ANZ slipped 1.6%.

The banks aren’t being helped by credit crunch headlines, as the fallout from the Royal Commission has resulted in banks imposing tougher lending assessment criteria. Quality borrowers are being either delayed getting, or denied, loans, which isn’t helping house prices and the future profitability of the banks. But the executive teams at the Big Four are running scared and not taking chances with their lending policies.

This is madness and I suggest the Treasurer, Josh Frydenberg, has to sort this out before it threatens the growth of the economy and the progress of stock prices.

Helping the local market has been the lift in commodities, with the AFR pointing out that “the Bloomberg Commodity index lifted to a two-month high.” As a consequence, it shouldn’t be a surprise that BHP sneaked up to a four-year high earlier in the week to end up 2.5% at $35.50.

Last week, I said our stock market was like that racehorse, Chautauqua, which refused to leave the barrier. Not much has changed. Trump and trade wars plus Hayne and credit threats, plus Shorten and his tough property, retiree and capital gains tax policies, are all brakes on stock market enthusiasm.

There were two notable developments during the week. One was the better-than-expected retail number, where the August 0.3% rise took the annual rise to 3.8%, which looks like it’s developing into a positive trend. And secondly, the lower dollar, which is now at 70.51 US cents and has nearly given up 2 cents over the week, which not only helps the stock prices of our exporters, it adds to economic growth.

What I liked

- Retail trade rose by 0.3% in August, after a flat outcome in July. Sales have lifted in seven out of eight months in 2018. Annual spending growth rose from 2.9% in July to 3.8% in August – the strongest growth rate in 15 months.

- The engineering PCI sub-index rose by 10.7 to 65.7 in September – the highest level since records began in September 2005. Engineering activity has expanded for 18 consecutive months.

- The trade surplus increased from $1,548 million in July (previously $1,551 million) to $1,604 million in August. It was the 13thsurplus in 15 months. Meat exports rose by $73 million to a record-high of $1,268 million in August.

- The CBA services sector gauge rose by 0.4 to 52.2 points in September. The employment sub-index hit five-month highs. Any reading over 50 indicates expansion.

- The ANZ-Roy Morgan consumer confidence rating rose by 0.8% to a 7-week high of 118.1 in the past week. The index is comfortably above the average of 114.1 held since 2014, and above the longer term average of 113 held since 1990.

- The estimate of family finances compared with a year ago stands at 8-month highs.

- The Commonwealth Bank/Markit purchasing managers survey for manufacturing rose from 53.2 to 54 in September. The index is above 50 points, suggesting expansion of the sector.

- The CoreLogic Home Value Index of capital city home prices fell by 0.6% in September to stand 3.7% lower over the year. The national home price index fell by 0.5% in the month, to be down 2.7% over the year. (I like the measured fall, with Sydney down 6.1% and Melbourne down 3.4% over the year.)

- The Australian Industry Group (AiGroup) Performance of Manufacturing Index rose from 56.7 points to 59 in September. The sector has been expanding – an index above 50 points – for the longest period since 2005.

- The ISM manufacturing index in the US eased from 14-year highs, dropping from 61.3 to 59.8 in September (forecast 60.1), but the levels are very good.

- Stock markets were optimistic on global trade after the US, Canada and Mexico signed a new trade deal.

- US factory orders rose by 2.3% (forecast: +2.1%) in August.

- The ADP employment report showed that 230,000 private sector jobs were created in September (forecast 185,000).

- The ISM services index for the US rose from 58.5 to 61.6 in September (forecast 58).

- There are signs that the Italian Government would target a smaller budget deficit and avoid conflict with the European Commission.

What I didn’t like

- In seasonally-adjusted terms, new detached house sales fell by 2.9% in August, following a 3.1% decline in July. And sales fell by 9.8% over the year.

- The Performance of Construction Index (PCI) eased to 49.3 in September, down from 51.8 in August – the first contraction in activity in 20 months. A reading above 50 points indicates construction activity is generally expanding; below 50, that it’s declining.

- The houses PCI sub-index fell 7.8 points to 42 in September – the lowest level in two years. Activity in the housing sector has contracted for two successive months.

- The national terminal gate (wholesale) unleaded petrol price stands at 142.9 cents a litre today, up 0.6 cents over the week at 4-year highs (highest since July 2014).

- News for chipmakers wasn’t great. Shares of Apple (-1.8%) and Amazon (-2.2%) fell on cybersecurity concerns, as both companies denied a Bloomberg report that their systems had been infiltrated by malicious computer chips inserted by Chinese intelligence. And chipmakers Micron (-2.2%) and Nvidia (-2.6%) shares fell after Deutsche Bank reduced its 2019 earnings forecasts.

Not Chautauqua, let’s have Winx

While Chautauqua won’t run, you have to hope we see our market get going like Winx, which competes at Flemington today, aiming for her 28th win in a row! Unfortunately, a winning run for the Oz stock market looks a way off yet but a falling dollar, an end to the trade war and certainty after the November 6 mid-term elections, could give us a chance to start a winning streak, though I can’t see it being Winx-like, even with all my positivity.

The Week in Review:

- Paul Rickard looked at the performance of our model portfolios [1] and found that, even though September was a rough month for the local market, they are holding their own.

- If you’re not sure whether to invest in one of the listed funds managers or to invest in the funds that the company manages, James Dunn looked at four companies, and the managed funds they operate [2], to work out which is the better investment.

- Head of research and portfolio manager at Pengana International Equities, Steven Glass, chose CME Group as the Stock of the Week [3].

- More and more NZ companies are crossing the ditch to list on the ASX, and Tony Featherstone looked at 5 dual-listed stocks ready to rocket [4].

- Analysts were not very active this week, with only three movements including an upgrade for St Barbara in this week’s Buy, Hold, Sell – what the brokers say [5].

- In Questions of the Week [6], we looked at why companies pay franking or imputation credits.

Top Stocks – how they fared:

What moved the market?

- Rising bond yields saw share markets fall.

- The new US Mexico Canada Agreement (USMCA) boosted the market, but tensions remain high between the US and China.

Calls of the week:

- Tony Featherstone believes [4] many more NZ companies will dual list on the ASX in the next decade.

- The federal government has directed the Australian Competition and Consumer Commission to investigate excessive foreign transaction fees.

- Nick ‘Honey Badger’ Cummins chose to not pick a winner on the season finale of The Bachelor.

The Week Ahead:

Australia

Monday October 8 — Job advertisements (September)

Tuesday October 9 — NAB business survey (September)

Wednesday October 10 — Consumer sentiment (October)

Wednesday October 10 — Building activity (June quarter)

Thursday October 11 — Speech by Reserve Bank official

Friday October 12 — Housing finance (August)

Friday October 12 — Credit & debit card data (August)

Friday October 12 — Financial Stability Review

Overseas

Monday October 1 — China Caixin services (September)

Tuesday October 2 — US NFIB Business Optimism (September)

Wednesday October 3 — US Producer price index (September)

Wednesday October 3 — US Monthly budget statement (September)

Thursday October 4 — US Factory orders (August)

Friday October 5 – US Non-farm payrolls (September)

Friday October 5 — US International trade (August)

Friday October 5 – US Non-farm payrolls (September)

Friday October 5 — US International trade (August)

Food for thought:

With pointed fangs I sit and wait;

with piercing force I crunch out fate;

grabbing victims, proclaiming might;

physically joining with a single bite. What am I?

Send in your answer to subscriber@switzer.com.au

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

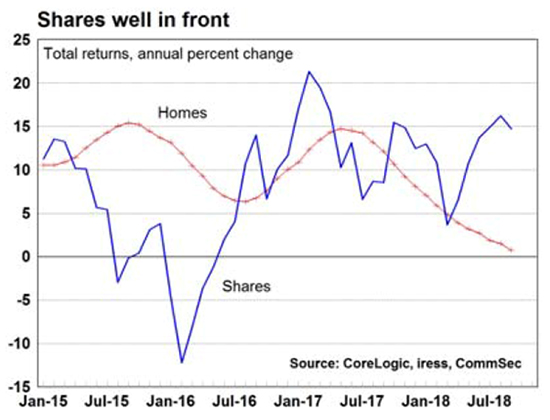

Chart of the week:

Total returns on shares are up almost 15% over the year, while residential property remains flat:

[7]Source: CoreLogic, IRESS, CommSec

[7]Source: CoreLogic, IRESS, CommSec

Top 5 most clicked:

- 5 dual-listed stocks ready to rocket [4] – Tony Featherstone

- 4 investment opportunities to weigh-up [2] – James Dunn

- Buy, Hold, Sell – what the brokers say [5]

- Switzer portfolios steady as market pulls back [1] – Paul Rickard

- Stock of the Week – CME Group [3] – Steven Glass

Recent Switzer Reports:

Thursday 4 October: Go like a rocket [8]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.