The Australian dental-services industry will grow a respectable 3.8% annually over 2014-19, estimates business forecaster IBISWorld. A growing, ageing population, and rising uptake of private health insurance is helping dentistry grow faster than the economy.

Growth drivers

The dental industry remains highly fragmented: about 70% of dentists still operate from one- or two-person practices, often in the suburbs. Listed dental companies see an obvious opportunity to consolidate or “roll-up” thousands of tiny practices into a corporate model.

Rising demand for cosmetic and restorative dental services is another growth driver. We once visited the dentist for an annual check-up and an occasional filing. Now, younger customers, in particular, have teeth whitened or straightened, creating revenue opportunities for dentists. They will even be able to pay for these services with Afterpay at some dentistry chains.

An improving Australian economy should be another fillip for the dental industry. There is a clear link between the economy’s strength and dental demand. When household budgets are pressured, consumers defer regular dental check-ups and discretionary treatments.

These trends suggest dental stocks should be doing okay, but listed dental stocks and dental-products providers have mostly had negative returns in the past 12 months. The good news is that after price falls this year, I sense some value returning to dentistry stocks.

The market’s largest dentistry stock, Pacific Smiles Group, has a three-year annualised average total return of minus 8.8%, Morningstar data shows. 1300 Smiles, one of the market’s better-run small-cap companies, has returned 2% annually over that period.

Share market newcomer Smiles Inclusive, an April 2018 Initial Public Offering (IPO), has given back early gains and is back near its $1 issue price, despite slightly upgrading its underlying earnings forecast in July, ahead of the statutory prospectus forecast.

Shares in Abano Healthcare Group, Australia’s second-largest dental group with 108 practices, have fallen about 15% this year. Abano, listed on the New Zealand Stock Exchange, reportedly wants to triple the business within a decade.

In dental products, micro-cap provider SDI has returned 2.6% annually over five years, Morningstar data shows. For context, the S&P ASX Small Ordinaries Accumulation index has returned 8.4% annually in this period.

Pass the pain killers to recent investors in dental stocks!

Beware roll-up hype

I have cautioned against “roll-up” stories several times in the Switzer Report in the past few years. The reality is that too many roll-up plays acquire firms too quickly and inevitably overpay for them. Or they take on too much debt, or issue too many shares to raise capital, diluting existing shareholders, including owners of firms acquired. Or they can not integrate small firms and their customers into a corporate culture.

As competition intensifies, valuations for privately owned firms rise. Small operators wanting to sell now have a few big firms competing to buy them. Anecdotally, that’s happening in dentistry with some operators reporting it’s harder to find value in the sector.

Lots of dentists like working for themselves in tiny practices and having control. They are more like self-employed professionals than growth-hungry small businesses. The risk of culture clashes between micro dental firms and giant dental corporates is significant. I can not imagine my local dentist, well into his 60s, taking orders from a corporate dental provider.

Health insurance is another risk if large funds form their own dental clinics (Bupa in Australia is a major dental provider) and steer patients away from preferred providers. Dentists who rely heavily on health-fund relationships could see some patients diverted to dental clinics owned or operated by large health-insurance providers, against which they cannot compete.

Against this backdrop, recent share-price weakness in dental stocks makes more sense.

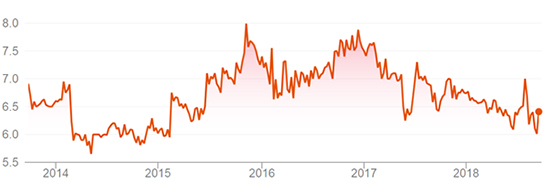

1300 SMILES (ONT)

I have followed the Townsville-based dental chain since it floated on the ASX in 2005, and rate its management and board highly. 1300 Smiles’ valuation has grown from $15 million at listing to $140 million. For a time, 1300 Smiles was among the best-performing small-cap stocks on ASX and known for its consistency.

1300 Smiles’ greatest strength – a conservative management approach – was probably its main weakness in the eyes of some analysts. I recall some lamenting to me that 1300 Smiles was too conservative with acquisitions: it needed to buy more firms each year and grow faster. I am glad the company resisted chasing growth for growth’s sake, and to please analysts.

Founder and CEO Daryl Holmes, a dentist, owns 62% of the shares, and runs 1300 Smiles like a family business. That is no criticism. The best small-cap companies over the years often have founders whose interests are strongly aligned with those of shareholders.

1300 Smiles’ FY18 profit result, released in August, caught my eye. The company added nine new dental practices, which is high by its standards and well up on the past few years. 1300 Smiles has a long record of walking away from acquisitions if they cost too much, therefore a boost in its acquisition strategy suggests the firm is seeing value re-emerge in dental practices.

1300 Smiles reported revenue growth of 9.6% to $55.8 million and 5% growth in net profit to $7.6 million for FY18.

Net profit as a percentage of statutory revenue, a key metric, was down slightly on the previous two years (at 19.4%). But with more acquisitions, I expected a larger fall, meaning 1300 Smiles is doing a good job on integrating acquired practices. A 4.3% rise in the dividend to 24 cents was another good sign.

This spike in 1300 Smiles’ acquisition rate sets it up for faster growth in FY19 and FY20, possibly more than the market expects. Normally, I’m wary when small firms lift their acquisitions run-rate, but 1300 Smiles has a good acquisition record.

Three broking firms that cover 1300 Smiles (too small to rely on) have an average price target of $6.92, suggesting the stock is a touch undervalued at the current $6.51.

1300 Smiles sold off after its FY18 result, but bargain hunters have been active this month. I see solid, rather than spectacular, gains ahead in the next two years for 1300 Smiles, which pioneered the listed dental-services model in Australia.

Chart 1: 1300 Smiles (ONT)

[1]Source: ASX

[1]Source: ASX

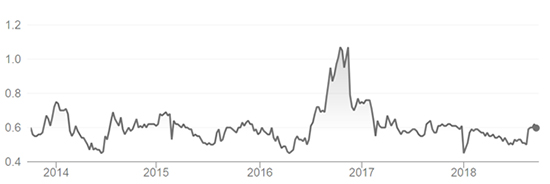

SDI (SDI)

Dental-products provider SDI is one to watch. As a thinly traded $71-million stock, SDI suits experienced investors who understand the risks of micro-cap investing.

Listed in 1985, SDI is Australia’s largest dental-products manufacturer. It makes a range of dental restorative products,

such as fillings and tooth-whitening products, and exports to more than 100 countries. Currency conversions have a big impact on its earnings.

SDI’s FY18 net profit rose 1.5% to $5.7 million. A stronger second half, where profit rose 27% on the same time last year, was a highlight.

Another was the reduction in amalgam sales as part of SDI’s sales mix. Demand for dental amalgam “silver fillings” is falling.

SDI’s balance sheet has strengthened. Cash rose by $2.5 million and debt fell by $1.9 million. The company has rising free cash flow and no net debts – traits I look for in small-cap stocks. An increased dividend and payout ratio are good signs, for they suggest the board is becoming more confident in SDI’s growth prospects.

I expect SDI to continue launching products that push it towards the growing aesthetics and tooth-whitening segments and away from commoditised materials for fillings, and other restorative work, that lower-cost countries are better placed to provide. Higher profit margins for SDI should result.

At 59 cents, SDI is on a trailing PE of 12 times and yielding 4.%, fully franked. They stock has rallied from a 52-week low of 42 cents.

SDI has many challenges, but demand for cosmetic dental products should continue to rise, as consumers in developed and emerging nations spend more money on teeth whitening and other dental aesthetics services.

SDI looks like it is returning growth as it transitions from a provider of more commoditised dental products to an innovative R&D firm with higher-value products for a global growth market.

Chart 2: SDI (SDI)

[2]

[2]

Source: ASX

Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor All prices and analysis at September 19, 2018.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.